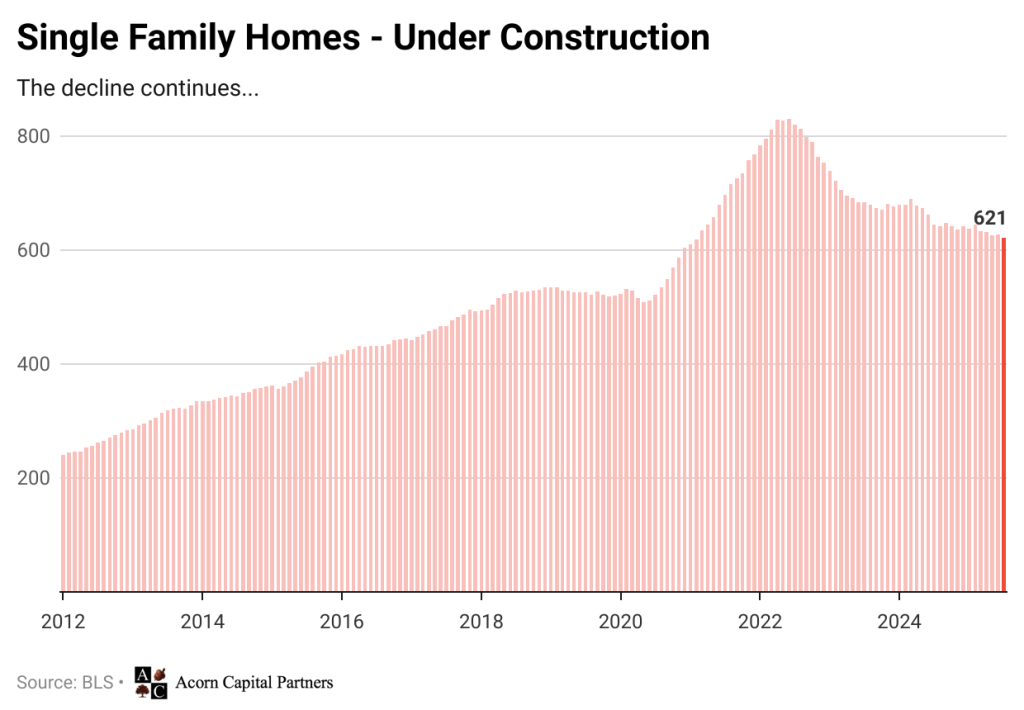

After months of resilience, U.S. home prices showed their first signs of softening this summer. In July, the national average slipped 0.1% compared with June, marking a modest but symbolically important shift. What makes this decline more significant is its reach: prices fell in 39 of the nation’s 50 largest metropolitan areas, indicating a broad cooling rather than a localized dip.

The pattern is not uniform across the country. High-cost regions on the West Coast and in the Mountain States are leading the pullback. These markets, already strained by some of the steepest affordability challenges in the country, are seeing buyers pull back as higher mortgage rates and elevated home values collide. In contrast, many markets in the Southeast and Midwest remain relatively steady, with some still posting gains. These regions are benefiting from in-migration, stronger affordability profiles, and limited housing stock that keeps competition for homes intact.

Mortgage rates remain the critical factor shaping the market. At current levels, they continue to price out many potential buyers, especially first-time entrants. This has created a stalemate: buyers are cautious, while homeowners remain reluctant to list their properties and give up lower locked-in rates. The result is a market that is cooling at the margins but still insulated from a deeper correction by historically low inventory.

For policymakers and investors alike, the takeaway is that housing remains under pressure, but not in freefall. The modest decline in July illustrates the fragile balance between constrained supply and affordability challenges. If rates stay elevated into the fall, further softening is likely. However, without a meaningful rise in housing supply, sharp price drops are unlikely.

Investor Implications

The latest housing data matters for investors across multiple sectors:

- Homebuilders (LEN, DHI, TOL, PHM): Even a small price dip raises questions about demand sustainability. Builders may face pressure on new sales unless mortgage rates ease, though inventory shortages could still support pricing power in affordable segments.

- REITs (EQR, AVB, CPT, MAA): Multifamily REITs could benefit if higher borrowing costs keep households renting longer. On the flip side, residential REITs tied to single-family rentals may face valuation pressure if home prices continue to soften.

- Mortgage Lenders & Banks (WFC, JPM, RKT): Elevated rates suppress refinancing and purchase volumes, limiting fee income. Smaller lenders with concentrated mortgage exposure may be particularly vulnerable.

- Building Materials & Retail (HD, LOW, SHW, MAS): Slower housing turnover tends to weigh on demand for remodeling and home improvement, though pent-up renovation projects can provide a buffer.

In short, July’s housing data suggests a sector under quiet strain. For investors, it’s a reminder that housing is not yet in crisis—but the balance of risk is shifting. If interest rates remain elevated into year-end, the gradual cooling could deepen, creating ripple effects across housing-related equities.